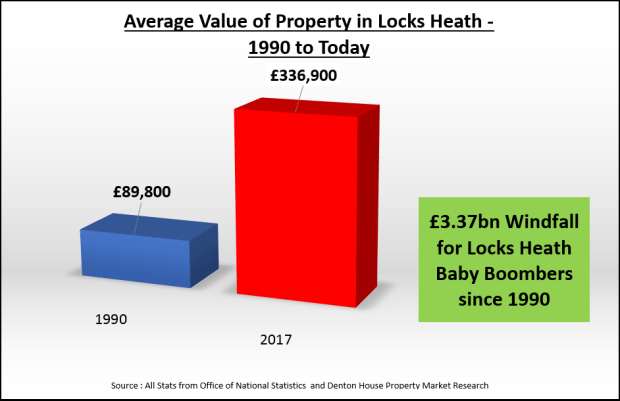

Well last week’s article “The Unfairness of the Locks Heath Baby Boomer’s £3,373,900,000 windfall?” caused a stir. In it we looked at a young family member of mine who was arguing the case that Millennials (those born after 1985) were suffering on the back of the older generation in Locks Heath. They claimed the older generation had seen the benefit of the cumulative value of Locks Heath properties significantly increasing over the last 25/30 years (which I calculated at £3.37bn since 1990). In addition many of the older generation (the baby boomers) had fantastic pensions, which meant the younger generation were priced out of the Locks Heath housing market.

Well last week’s article “The Unfairness of the Locks Heath Baby Boomer’s £3,373,900,000 windfall?” caused a stir. In it we looked at a young family member of mine who was arguing the case that Millennials (those born after 1985) were suffering on the back of the older generation in Locks Heath. They claimed the older generation had seen the benefit of the cumulative value of Locks Heath properties significantly increasing over the last 25/30 years (which I calculated at £3.37bn since 1990). In addition many of the older generation (the baby boomers) had fantastic pensions, which meant the younger generation were priced out of the Locks Heath housing market.

I replied there should be no surprise though that the older members of our society hold considerably more of our country’s wealth than the younger generation. This wealth is accrued and saved across someone’s life, and reaches it’s peak about the time of retirement. If we are to comprehend differing wealth levels between generations we need to compare ‘apples with apples’. It is much more important to track the wealth held by different generations at the same age, i.e. what was ‘real’ wealth of the 30-something couple in the 1960’s compared to a 30-something couple say in the 1980’s or 2010’s?

So could it be all about these people saving? The fact is, in the last 10 years, UK households have saved on average 7.5% to 8% of the household income into savings accounts, compared to an average of 6% to 7% in the late 1960’s and 1970’s. The baby boomers haven’t been actively squirreling away their cash for the last 30 or 40 years in savings accounts to accumulate their wealth. Most of their gains have been passive, lucky bonuses gained on the back of things out of their control (unanticipated and massive property value rises or people living longer making final salary pensions more valuable) – it’s not their fault!

… and herein lies the issue… it is assumed that these Millennials aren’t buying property in the same numbers like the older generation did in the past (because most of their wealth has come from house price inflation). The Millennials have often been described as ‘Generation Rent’, because they rent as opposed to buying property – because we are told they can’t buy.

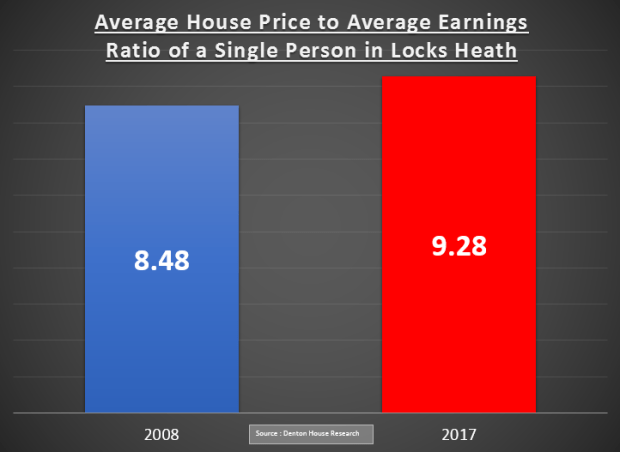

However, when Locks Heath mortgage payments are measured against monthly income, home ownership is affordable by historic standards because mortgage rates are currently so low. As you can see, the ratio of average house price to average earnings in Locks Heath hasn’t vastly changed over the last decade…

- 2008 average house price to average earnings of a single person in Locks Heath 8.48 to 1

- 2017 average house price to average earnings of a single person in Locks Heath 9.28 to 1

(i.e. in 2008, the average house price in Locks Heath was 8.48 times more than the average person’s salary in Locks Heath and this has only risen to 9.28 in 2017 – and all this off the property boom of the early 2010’s)

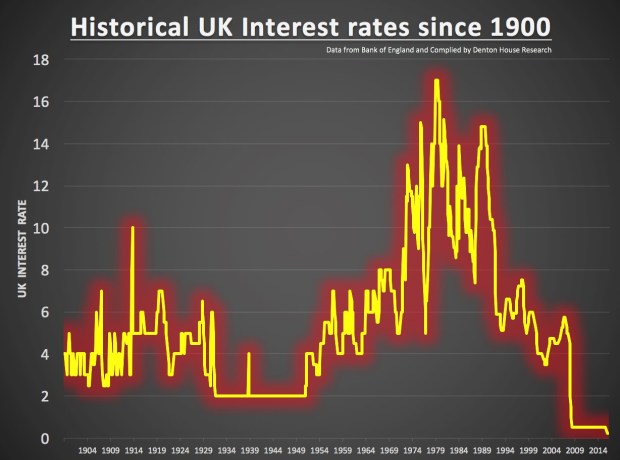

95% first-time buyer mortgages were reintroduced in 2010. The average interest rate charged for those 95% FTB mortgages has slowly dropped from around 5.5% in 2009 to the current 4% rate. Back in the 1980’s/1990’s mortgage interest rates were between 8% and 10%, and one time in the early 1990’s, reached 15%! The main difference between the two periods was the absolute borrowing relative to income is greater now than in the 1980’s. They call this the ‘mortgage to joint household income ratio’. In the 1980’s the mortgage was between 1.8x to 2x joint income; today it is 3.4x to 3.6x salary.

The simple fact is, in the majority of cases, it is still cheaper for a first-time buyer to buy a property with a 95% mortgage, than it is rent it. The barrier for these Millennials, has to be finding the 5% mortgage deposit – instead of being able to afford monthly mortgage outgoings at the current 95% mortgage rates?

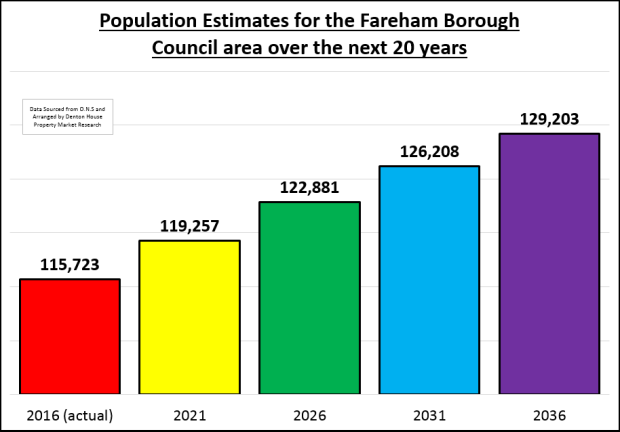

Millennials make up 5,279 households in the Fareham Borough Council area (or 11.33% of all households in the area). However, behind the doom and gloom, surprisingly, 48.2% did save up the 5% deposit and do in fact own their own home (that surprised you didn’t it!)

Nonetheless, the majority of Millennials in the area still do rent from a Landlord (1,910 Millennial households to be exact). Yet, they have a choice. Buckle down and do what their parents did and go without the nice things in life for a couple of years (i.e. the holidays, out on the town two times a week, the annual upgraded mobile phones, the £100 a month Satellite packages) and save for a 5% mortgage deposit… or live in a lovely rented house or apartment (because they are nowadays), without any maintenance bills and live a life with no intention of buying (because renting doesn’t have a stigma anymore like it did in the 1960’s/70’s (secretly hoping their parents don’t spend all their inheritance so they can buy a property later in life – like they do in central Europe).

Neither decision is right or wrong although it is still a choice. Until Millennials decide to change their choices – that is the reason why the country’s private rental sector will continue to grow for the next 30 years – meaning happy Tenants and happy Landlords.

Recently I was having a chat with one of my older relatives at a big family get-together. We and a couple of their children got talking over a drink about the times of 15% interest rates and how the more mature members of our family had to endure the 3 day week, 20% inflation and the threat of nuclear annihilation in 4 minutes. So, foolishly, my older relative said what with all the opportunities youngsters had today, they had never had it so good!

Recently I was having a chat with one of my older relatives at a big family get-together. We and a couple of their children got talking over a drink about the times of 15% interest rates and how the more mature members of our family had to endure the 3 day week, 20% inflation and the threat of nuclear annihilation in 4 minutes. So, foolishly, my older relative said what with all the opportunities youngsters had today, they had never had it so good!

On several occasions over the last few months, in my Locks Heath Property Blog, I predicted that the rate of rental inflation (i.e. how much rents are rising by) had eased over the last year. At the same time I felt that in some parts of the UK rents had actually dropped for the first time in over eight years. Recent research backs up this prediction.

On several occasions over the last few months, in my Locks Heath Property Blog, I predicted that the rate of rental inflation (i.e. how much rents are rising by) had eased over the last year. At the same time I felt that in some parts of the UK rents had actually dropped for the first time in over eight years. Recent research backs up this prediction.

50 years ago, in 1967, the first human heart transplant was performed by Dr Christian Barnard in South Africa. In the same year Sweden switched from driving on the left-hand side to the right-hand side of the road. The average value of a Locks Heath property was £4,845, interest rates were at 5.5% and The Beatles released one of my favourite albums – their Sgt Pepper album… but what the hell has that to do with the Locks Heath property market today?? Quite a lot actually… so with my music turned up loud, let me explain my friends!

50 years ago, in 1967, the first human heart transplant was performed by Dr Christian Barnard in South Africa. In the same year Sweden switched from driving on the left-hand side to the right-hand side of the road. The average value of a Locks Heath property was £4,845, interest rates were at 5.5% and The Beatles released one of my favourite albums – their Sgt Pepper album… but what the hell has that to do with the Locks Heath property market today?? Quite a lot actually… so with my music turned up loud, let me explain my friends!