What is your greatest fear as a Landlord? Like most it is more than likely a Tenant either not paying the rent or trashing the property.

So how do you avoid the pitfalls and ensure that you give yourself the best chance of getting yourself a good Tenant?

Here I detail my 7 Top Tips to help you find the best Tenant for your property.

1. Make sure you carry out background checks

If you are going to be letting a Tenant live in your property you want to make sure that they have the income or savings to pay you every month. Proof of income can be in the form of confirmation from an employer or accountant, payslips or bank statements.

You also want to know what sort of Tenant they have been in their previous property that they have been renting so get their current Landlord or Agent’s information and contact them for some details of their tenancy. Some good questions to ask are:

- Have they paid their rent on time and in full each month?

- Did they leave the property in good condition at the end of their tenancy?

- Would they let to them again?

Needless to say that the sure-fire method of carrying out background checks is through a professional referencing agency. But if you are doing the checks yourself don’t be afraid to be intrusive and ask some detailed questions to ensure you have the full picture on your prospective Tenant.

2. Avoid Facebook groups

We all like to save some money and Facebook has become a very popular medium for us to buy or sell second hand goods. ‘For Sale in….’ groups have popped up for most local small towns and villages and Landlords have turned to these to advertise their properties. But before you take your photos and upload them to your local Facebook Group there is something you need to consider… Are you going to be attracting the best quality Tenant?

Some prospective Tenants are legitimately looking to save some money on fees by going to a private Landlord. Sadly however there are also a lot of Tenants with chequered pasts that resort to Facebook because they know that full referencing checks will not be carried out. The warning signs may not be there at first; they may come across really well at your face to face meeting at the property but once that agreement is signed and they have moved in things can quickly change.

3. Have the right legal documents in place

Having the right tenancy agreement is essential when letting your property. Without the right clauses protecting you you could end up with no recourse should the Tenant let you down.

Always ensure that you use a properly written and legally binding contract. If your proposed tenancy is eligible you should always use an Assured Shorthold Tenancy.

4. Take a deposit and handle it correctly

Typically in the SO31, PO14 or PO15 areas a deposit of between one month and six weeks’ rent is taken from Tenants. Needless to say that this should be paid by your Tenants in cleared funds prior to you handing over any keys.

To comply with Deposit Legislation the deposit should be registered with a government recognised Deposit Protection Scheme and prescribed information regarding the deposit should be issued to the Tenants all within 30 days.

The deposit will remain protected until the end of the tenancy and will protect you against any damages to the property or the contents. In the event of a dispute between you and your Tenant the Deposit Scheme will adjudicate.

5. Carry out an Inventory

In correlation with the deposit it is essential that you prepare an Inventory on the condition of the property and the contents. This should include a full list of all fixtures, fittings and furnishings and some photographs showing them.

The Inventory should make reference to any existing defects, blemishes and wear and tear. You and the Tenant should both sign the document on the day of occupation to confirm agreement that the document is a fair representation of the condition of the property.

Although it is an additional expense to an already long list of upfront costs I would always recommend getting an independent third party to prepare a professional Inventory. This keeps everything impartial and free from any bias.

My article on the importance of an Inventory goes in to more detail on this subject. CLICK HERE to read more.

6. Take ID and carry out a Right to Rent Check

It goes without saying that you want to be sure that your Tenant is who they say they are. But the Immigration Act 2014 and 2016 now takes that a step further by stipulating that Landlords must ensure that their tenants have a ‘right to rent’ – the right to remain in the UK. This means that you must carry out Right to Rent checks on all prospective adult occupiers.

Establish who will live in the property. Obtain, Check and Copy one or more original documents that demonstrate the Right to Rent in the UK for all adult occupiers for that property in the presence of the holder. Acceptable documents include a UK passport and a permanent residence card or travel document showing indefinite leave to remain.

Landlords must also carry out follow up checks where tenants satisfied initial checks using time limited ID.

7. Trust your gut instinct

Although credit checks and other references from employers can confirm whether the Tenant is financially sound it doesn’t necessarily guarantee that they will be a good Tenant.

First impressions count for a lot and your face to face meeting with the Tenant on the viewing is the ideal time to chat to them and get a feeling for what type of person they are.

Trust your gut instinct and if you are the slightest bit unsure about the Tenants do not agree to let to them and keep looking.

If you would like any more information or would like to discuss any other property related matter please give me a call on 01489 570011. You can also email me at james.hill@brooklettings.co.uk.

For more articles like this one and all the latest buy to let deals for investors visit The Locks Heath Property Blog.

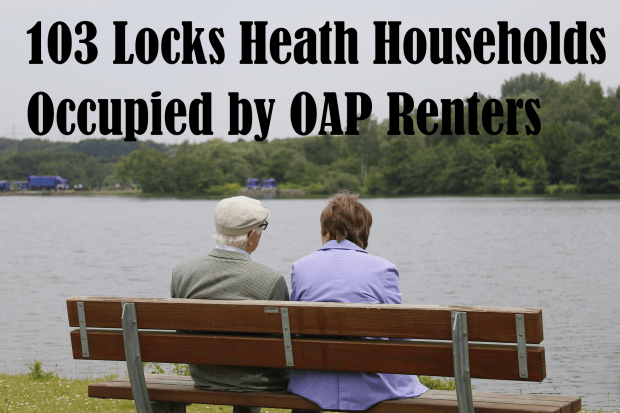

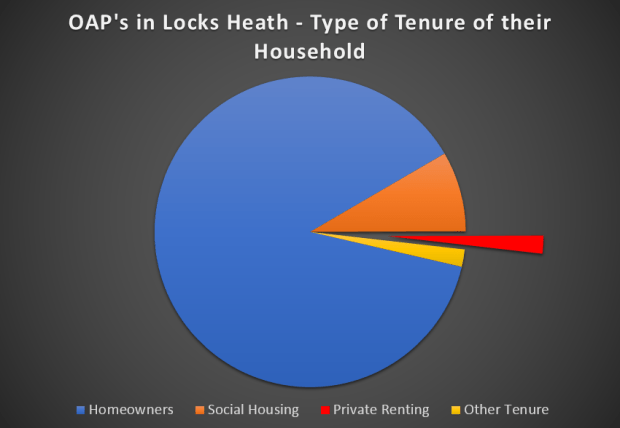

Recent statistics published by the Office of National Statistics show that there are 267,704 private rented households in the Country that are occupied by people aged 65 and older, meaning 4.39% of OAP’s are living in private rented property.

Recent statistics published by the Office of National Statistics show that there are 267,704 private rented households in the Country that are occupied by people aged 65 and older, meaning 4.39% of OAP’s are living in private rented property.

Can we blame the 55 to 70-year-old Locks Heath citizens for the current housing crisis in the town?

Can we blame the 55 to 70-year-old Locks Heath citizens for the current housing crisis in the town?

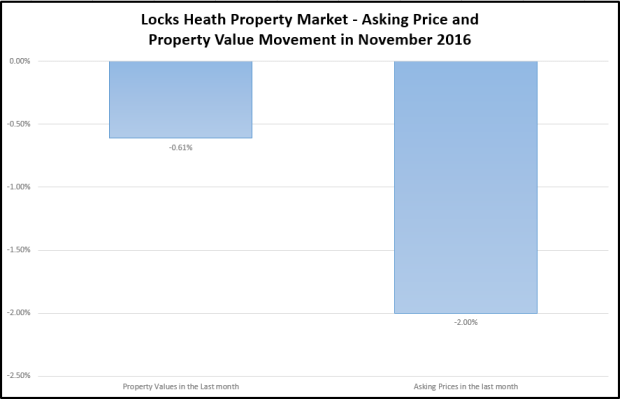

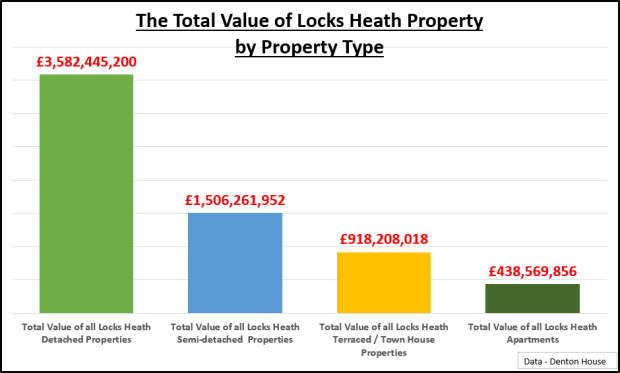

While Brexit has not yet had a sizeable impact on the Locks Heath housing market, my analysis is pointing to the fact that the economic viewpoint still remains uncertain and Locks Heath property price growth is likely to be more subdued in 2017 – although that isn’t a bad thing so let me explain.

While Brexit has not yet had a sizeable impact on the Locks Heath housing market, my analysis is pointing to the fact that the economic viewpoint still remains uncertain and Locks Heath property price growth is likely to be more subdued in 2017 – although that isn’t a bad thing so let me explain.

Well, hasn’t 2016 been eventful. The ups and downs of Brexit, the Queen’s 90th, Andy Murray winning Wimbledon, Trump, Bake Off to Channel 4 and something close to the hearts of every buy to let Landlord and homeowner in Locks Heath … the Locks Heath property market.

Well, hasn’t 2016 been eventful. The ups and downs of Brexit, the Queen’s 90th, Andy Murray winning Wimbledon, Trump, Bake Off to Channel 4 and something close to the hearts of every buy to let Landlord and homeowner in Locks Heath … the Locks Heath property market.