A little bit of good news this week on the Locks Heath Property Market as recently released data shows that the number of first time buyers taking out their first mortgage in 2017 increased more than in any other year since the global financial crisis in 2009. The data shows there were 54 first time buyers in Locks Heath, the largest number since 2006.

A little bit of good news this week on the Locks Heath Property Market as recently released data shows that the number of first time buyers taking out their first mortgage in 2017 increased more than in any other year since the global financial crisis in 2009. The data shows there were 54 first time buyers in Locks Heath, the largest number since 2006.

I expect in 2018 that this increase of first time buyers will level out and maybe dip slightly as, nationally, figures demonstrate that first time buyer’s average household income was £40,691 and this represented 17.3% of their take home pay. Although, it might surprise readers that it is actually cheaper to buy than it is to rent at the ‘starter home’ end of the housing market. Many of you can remember mortgage rates at 12%… even 15%. Today, at the time of writing this article, I found on the open market, 189 first time buyer mortgages at 95% (meaning only a 5% deposit was required) with 3 year fixed rates from a reputable High Street bank at 2.49%… they even did a 3 year fixed rate 100% mortgage for 2.89%!

Interestingly, looking at the other end of the market, the buy-to-let investment in Locks Heath was subdued, with only 11 buy-to-let properties being purchased with a mortgage. However, I must stress, whilst there is no hard and fast data on the total numbers of Landlords buying buy-to-let, as HM Treasury believes only 30% to 40% of buy-to-let property is bought with a mortgage. This means there would have been further cash only buy-to-let purchases in Locks Heath – it’s just that the data isn’t available at such a granular level.

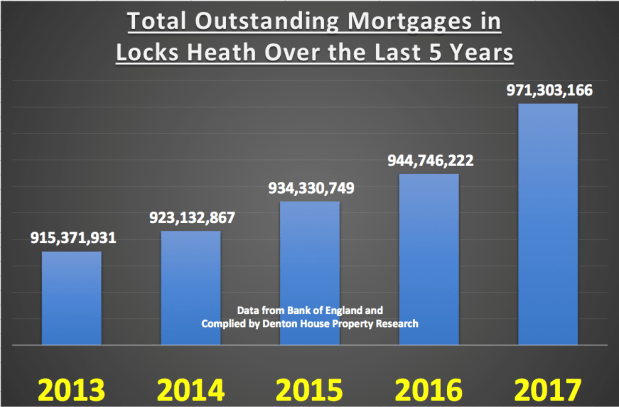

In terms of the level of mortgage debt in Locks Heath, looking specifically at the SO31 postcode, you can see there has been a steady rise in borrowing over the last few years.

This is pleasing to see, as new mortgage debt is created by first time buyers, buy-to-let landlords and home movers themselves, that is being roughly equalled by the amount being paid off with mature mortgaged homeowners in their 50’s and 60’s finally paying off their mortgage.

So, what does all this mean for the Locks Heath Property Market? Well, the stats paint a picture, but they don’t inform us of the whole story. The upper end of the Locks Heath property market has been weighed down by the indecision around the Brexit negotiations and rise in stamp duty in 2014, when it made it considerably more expensive to buy a home costing more than £1m. The middle part of the Locks Heath property market has been affected by issues of mortgage affordability and lack of good properties to buy, as selling prices have reached the limit of what buyers can afford under existing mortgage regulations. The lower to middle Locks Heath property market was hit by tax changes for buy-to-let landlords, although this has been offset by the increase in first time buyers.

If you are in the market and selling now and want to ensure you get your Locks Heath property sold, the bottom line is you have to be 100% realistic with your pricing from day one and you might not get as much as you did say a year ago (but the one you want to buy will be less – swings and roundabouts?). I know it’s not comfortable hearing that your Locks Heath home isn’t worth as much as you thought, but Locks Heath buyers are now unbelievably discerning.

So, if you are thinking of selling your Locks Heath property in the coming months, don’t ask the agent out a few days before you want to put the property on the market, get them out now and ask them what you need to do to ensure you get maximum value in the shortest possible time.

That got your attention … didn’t it!

That got your attention … didn’t it!

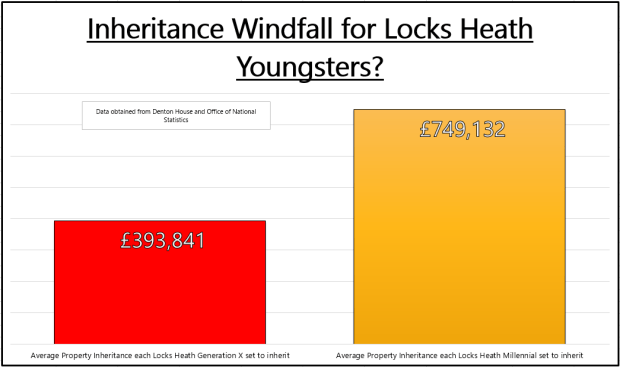

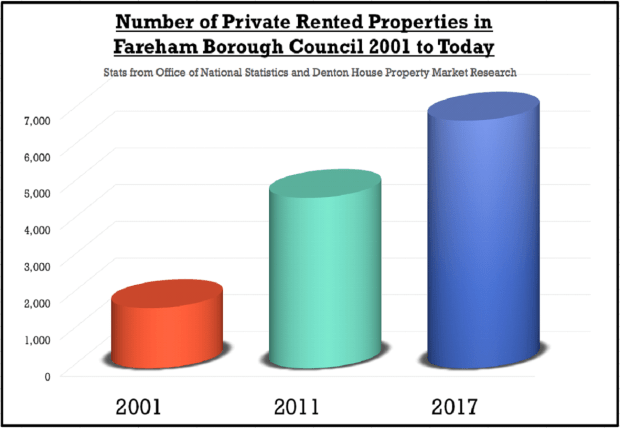

Yes, I said ‘rentirement’, not retirement… rentirement, and it relates to the 397 (and growing) Locks Heath people, who don’t own their own Locks Heath home but rent their home, privately from a buy to let Landlord and who are currently in their 50’s and early to mid-60’s.

Yes, I said ‘rentirement’, not retirement… rentirement, and it relates to the 397 (and growing) Locks Heath people, who don’t own their own Locks Heath home but rent their home, privately from a buy to let Landlord and who are currently in their 50’s and early to mid-60’s. As I am sure you are aware, one the best things about my job as an agent is helping Locks Heath Landlords with their strategic portfolio management. Gone are the days of making money by buying any old Locks Heath property to rent out or sell on. Nowadays, property investment is both an art and science. The art is your gut reaction to a property, but with the power of the internet and the way the Locks Heath property market has gone in the last 11 years, science must also play its part on a property’s future viability for investment.

As I am sure you are aware, one the best things about my job as an agent is helping Locks Heath Landlords with their strategic portfolio management. Gone are the days of making money by buying any old Locks Heath property to rent out or sell on. Nowadays, property investment is both an art and science. The art is your gut reaction to a property, but with the power of the internet and the way the Locks Heath property market has gone in the last 11 years, science must also play its part on a property’s future viability for investment. As head in to the second month of 2018 I believe UK interest rates will stay low, even with the additional 0.25% increase that is expected in May or June. That rise will add just over £20 to the typical £160,000 tracker mortgage, although with 57.1% of all borrowers on fixed rates, it will probably go undetected by most buy-to-let Landlords and homeowners. I forecast that we won’t see any more interest rate rises due to the fragile nature of the British economy and the Brexit challenge. Even though mortgages will remain inexpensive, with retail price inflation outstripping salary rises, it will still very much feel like a heavy weight to some Locks Heath households.

As head in to the second month of 2018 I believe UK interest rates will stay low, even with the additional 0.25% increase that is expected in May or June. That rise will add just over £20 to the typical £160,000 tracker mortgage, although with 57.1% of all borrowers on fixed rates, it will probably go undetected by most buy-to-let Landlords and homeowners. I forecast that we won’t see any more interest rate rises due to the fragile nature of the British economy and the Brexit challenge. Even though mortgages will remain inexpensive, with retail price inflation outstripping salary rises, it will still very much feel like a heavy weight to some Locks Heath households.

I was recently reading a report by the Home website which suggested that hordes of Landlords are selling their buy-to-let investments due to increasing burdens on them in the buy-to-let market. Their findings suggest the number of new properties that came onto the market nationally (for sale) jumped by 11% across the UK as a result.

I was recently reading a report by the Home website which suggested that hordes of Landlords are selling their buy-to-let investments due to increasing burdens on them in the buy-to-let market. Their findings suggest the number of new properties that came onto the market nationally (for sale) jumped by 11% across the UK as a result.

Talk to many Locks Heath 20 something’s, where home ownership has looked but a vague dream, many of them have been vexatious towards the Baby Boomer generation and their pushover ‘easy go lucky’ walk through life; jealous of their free university education with grants, their eye watering property windfalls, their golden final salary pensions and their free bus passes.

Talk to many Locks Heath 20 something’s, where home ownership has looked but a vague dream, many of them have been vexatious towards the Baby Boomer generation and their pushover ‘easy go lucky’ walk through life; jealous of their free university education with grants, their eye watering property windfalls, their golden final salary pensions and their free bus passes.

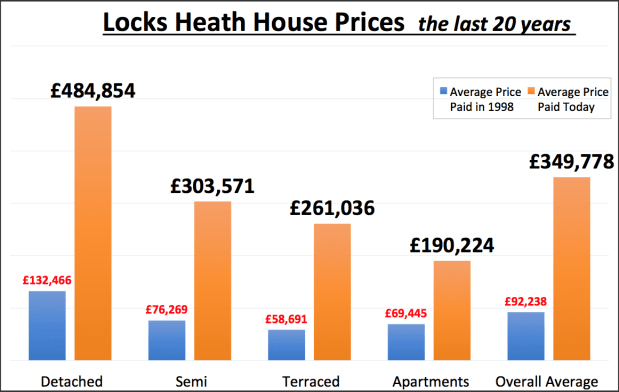

My research shows that certain types of Locks Heath property are more affordable today than before the 2007 credit crunch.

My research shows that certain types of Locks Heath property are more affordable today than before the 2007 credit crunch.